Deduction of Income tax at source for 2019-2020

Income Tax to be deducted from income for the financial year 2019-20 (Assessment Year 2020-21) as per Finance Act. 2019

MINISTRY OF DEFENCE

Office of the JS & CAO

Deduction of income tax at source for the financial year 2019-2020

1. As per the Govt. orders, the recovery of tax, as due, from the Pay and Allowances of the employees is required to be ensured by the respective DDOs. As prescribed under income tax Act, the deduction of tax every month on proportionate basis is being made by the Admin sections for the current financial year 2019-20 in majority of cases. Further recoveries if any, are to be regulated in respect of each employee in the ensuing months i.e. in Pay bills for the months of Nov 2019 to Feb 2020.

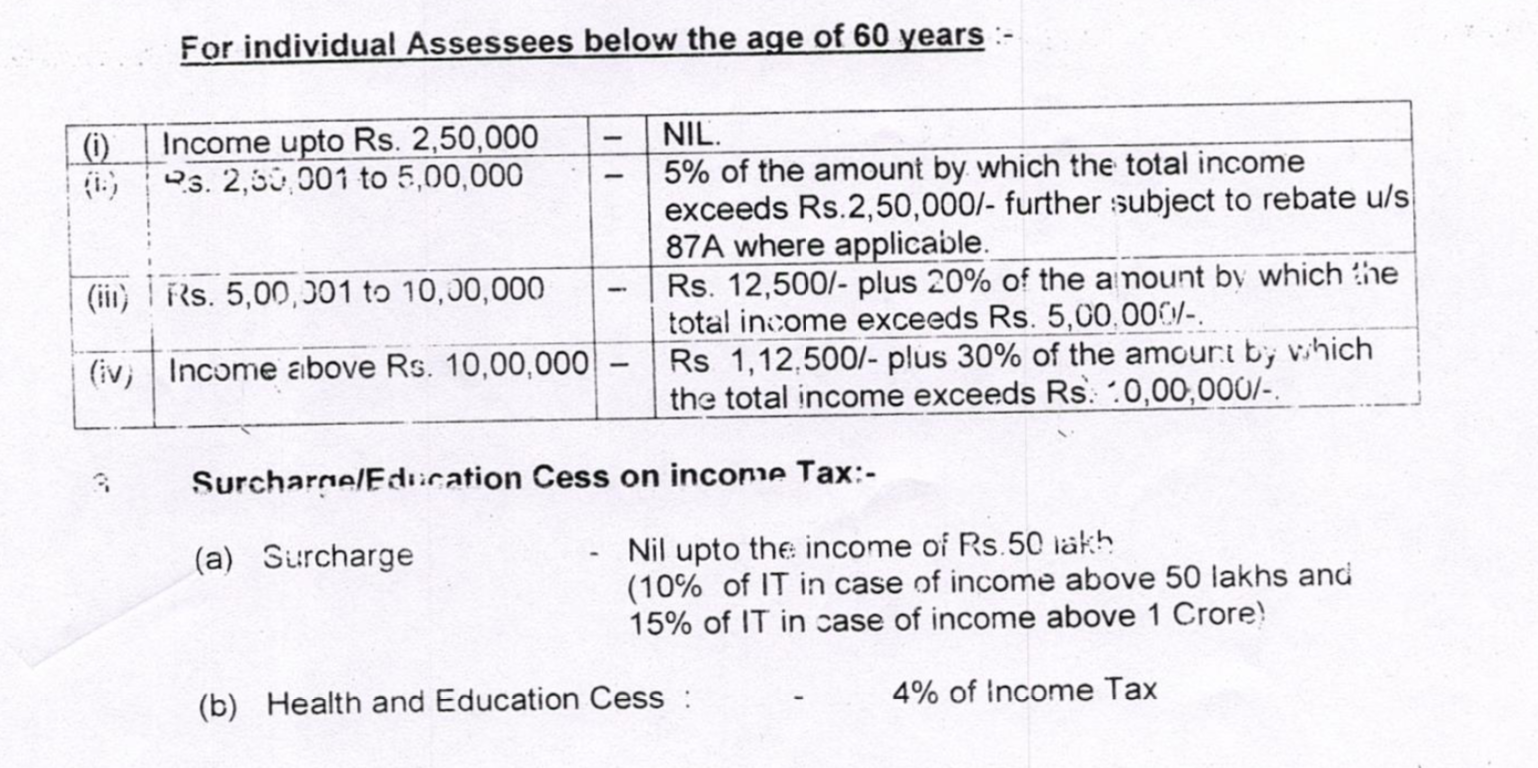

2. According to the Finance Act. 2019, Income Tax is required to be deducted from

income for the financial year 2019-20 (Assessment Year 2020-21) at the following rates:-

3. Salient features under Finance Act 2019 relevant for Salaried class :-

The following amendments have been made to the existing. provisions effective from Financial Year 2019-20.-

(i) Standard Deduction: Standard Deduction u/s 16 (ia) is enhanced ; Rs.50,000/- for the Financial Year 2019-20. The benefit of increase ?d standard deduction shall be available to salaried persons and pensioners.

(ii) Amendment in rebate u/s 87A : Rebate of Income Tax u/s 87A in case of certain individual where net taxable income is upto Rs.5 Lac (previous year Rs.3.5 Lac), there will be no income to .): for the FY 2019-20. Further, if taxable income marginally exceeds the limit of Rs. 5 Lakh, there will be no rebate of Income Tax under this section.

(ii) income from House Property : There is amendment in Sections 23 where tax payer is allowed to opt two house as self-occupied house (earlier it was allowed for only one house) and remaining house(s), if any has to be shown as let out. U/s 24, the tax payer, can now claim interest for both the house. However, the aggregate monetary limit of the deduction would remain the same i.e. Rs.2,00.000/-

5. it is stated that as per the revised format of Form-16, a new column i.e. “Reported

total amount of Salary received from other employer (s)”under the head of Salaries has been added. Accordingly, as per Sub Section 2 of Section 192 of Income Tax Act; on change of-employment the particulars of salary and TDS of earlier employment is required to be furnished by the employee to the subsequent employer. These particulars are to be furnished in Form-12B (copy enclosed) in accordance with Rule 26A of the Income Tax Rules. Hence, all officials who drew their salary from any office other than CAO in the FY 2019-20 are required to furnish Form-12B also.

6. All officials whose income exceeds Rs.2,50,000/- during the financial year 2019-20 are required to report their details of savings except GPF/NPS contribution as per Pro-forma enclosed to their respective Admin sections latest by 31 Oct 2019 positively along with relevant documents failing which the tax will be calculated by this office and recovered from Regular Pay Bills of Nov 2019 to Feb 2020

7. It is compulsory for all whose income under Sec192 of IT Act is above taxable

limit to furnish PAN to the deductor even though the tax payable is NIL. Such employees, who have not yet obtained the PAN should apply for the same immediately and intimate their PAN as early as possible. It may be noted that a penalty of Rs 10,000/-has been prescribed under Income Tax Act for wilfully intimating a false PAN. if an employee fails to furnish his/her PAN to the dedicator, TDS will be deducted at higher rates.

8. The contents of this note may be disseminated to all concerned for information and strict compliance.

Read / Download Deduction of Income-tax at source for 2019-2020

Also check the following links related to the latest income tax calculators

Income Tax Calculator 2019-20 – With Save Option And Instant Version

📢 Stay Updated with GConnect

Join our Whatsapp channels for the latest news and job updates:

Join GConnect News Join GConnect Jobs

GConnect News

GConnect Jobs