What is Gross Salary and How is it Computed

1.1. WHAT IS “ GROSS SALARY” AND HOW IT IS COMPUTED ?

Any amount received by an Employee from an Employer is known as Salary. To receive / give salary, there was to be an Employee-Employer relationship.

What is GROSS SALARY according to Income-Tax?

GROSS SALARY means :

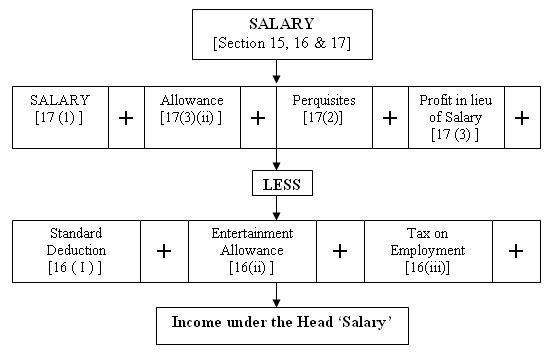

1. Basic Salary or Wages, Bonus, Pension, Gratuity (beyond exempted limit), Leave Salary or encashment, Advance Salary, Salary arrears, Fee or Commission, Remuneration for extra work, Ex-gratia, Award for excellence etc.

2. Allowances such as House Rent Allowance, Dearness Allowance, City Compensatory Allowance, Children’s Education Allowance, Conveyance Allowance, Fixed Medical Allowance and any other Special Allowances.

3. Perquisites – viz., Rent Free Accommodation, Amount spent or paid by the Employer on behalf of the Employee in respect of Gas, Electricity, Water Charges, Children’s School Fee, Club Fees, etc.

4. Benefit received in place of Salary which includes Retrenchment Compensation (Amount given to an employee when his services are no more required).

5. Pension received from former Employer is taxable as “Salaries”. However, Family Pension is taxed as income from other sources and is eligible for deduction up to Rs.15,000 or 33.33% whichever is less u/s 57 (ii a).

However Gross Salary does not include :

(1) Retirement Gratuity / Death Gratuity u/s 10(10)

(2) Sumptuary Allowance

(3) Medical treatment Reimbursement (with restrictions)

(4) Leave Travel Concession

(5) Uniform Allowance

(6) Leave encashment at retirement u/s 10(10AA)

(7) Free Meals / Refreshment provided during office hours.

How Salary is Computed :

This can be depicted in the form of Chart given below

📢 Stay Updated with GConnect

Join our Whatsapp channels for the latest news and job updates:

Join GConnect News Join GConnect Jobs

GConnect News

GConnect Jobs